1. EU Goals[1]

Under the Green Deal of the European Union, EU aims to become the first continent that removes as many CO2 emissions as it produces by 2050. This goal will become legally binding if the European Parliament and Council adopt the new Climate Law. The EU’s interim emission reduction target for 2030 would also be updated from the current 40% reduction to a more ambitious one.

On 7 October 2020, the European Parliament backed climate neutrality by 2050 and a 60% emission reduction target by 2030 compared to 1990 levels - more ambitious than Commission’s proposal of 55%. Members of the European Parliament are calling for the Commission to set an additional interim target for 2040 to ensure progress towards the final goal.

In addition, members called for all EU countries individually to become climate neutral and insisted that after 2050, more CO2 should be removed from atmosphere than is emitted. Also, all direct or indirect subsidies to fossil fuels should be phased out by 2025 at the latest.

Currently five EU countries have set the target of climate neutrality in law: Sweden aims to reach net-zero emissions by 2045 and Denmark, France, Germany and Hungary by 2050.

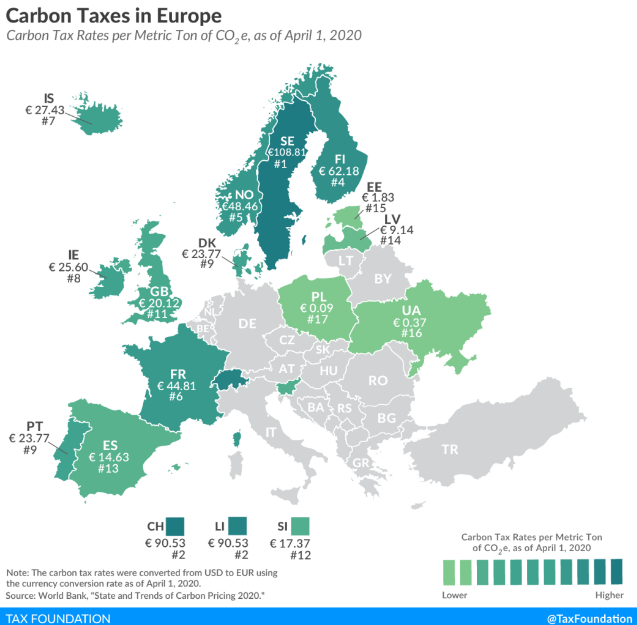

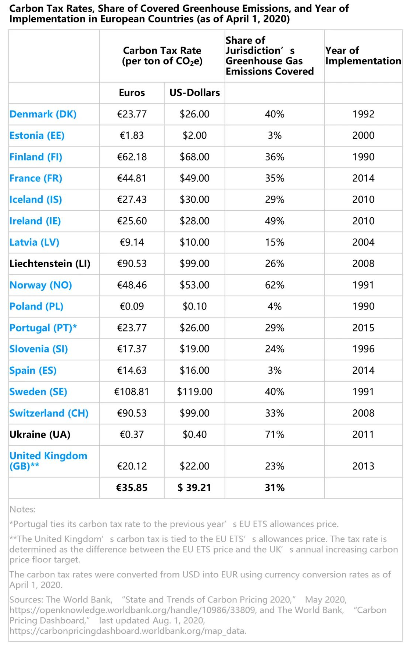

2. Carbon Taxes in Europe[2]

In recent years, several countries have taken measures to reduce carbon emissions using environmental regulations, emissions trading systems (ETS), and carbon taxes. In 1990, Finland was the world’s first country to introduce a carbon tax. Since then, 16 European countries have followed, implementing carbon taxes that range from less than €1 per metric ton of carbon emissions in Ukraine and Poland to over €100 in Sweden.

Sweden levies the highest carbon tax rate at €108.81 (US $119) per ton of carbon emissions, followed by Switzerland and Liechtenstein (€90.53, $99) and Finland (€62.18, $68). People will find the lowest carbon tax rates in Poland (€0.09, $0.10), Ukraine (€0.37, $0.40), and Estonia (€1.83, $2).

Carbon taxes can be levied on different types of greenhouse gases, such as carbon dioxide, methane, nitrous oxide, and fluorinated gases. The scope of each country’s carbon tax differs, resulting in varying shares of greenhouse gas emissions covered by the tax. For example, Spain’s carbon tax only applies to fluorinated gases, taxing only 3 percent of the country’s total greenhouse gas emissions. Norway, by contrast, recently abolished most exemptions and reduced rates, now covering over 60 percent of its emissions.

All member states of the European Union (plus Iceland, Liechtenstein, and Norway) are part of the EU Emissions Trading System (EU ETS), a market created to trade a capped number of greenhouse gas emission allowances. With the exception of Switzerland and Ukraine, all European countries that levy a carbon tax are also part of the EU ETS. (Switzerland has its own emissions trading system, which is tied to the EU ETS since January 2020.)

Several European countries are currently considering or have announced the implementation of a carbon tax or an ETS. For example, Germany will implement a national ETS for the heat and road transport sectors—both not covered by the EU ETS—in January 2021. Luxembourg plans to implement a €20 ($22) per ton of CO2 carbon tax in 2021, and Austria has announced its intention to introduce some form of carbon pricing.

3. European Union Emissions Trading Scheme[3]

The European Union Emissions Trading Scheme (EU ETS) is the world’s first and so far the largest installation-level ‘cap-and trade’ system for cutting greenhouse gas (GHG) emissions. The system is intended to assist the EU in reaching both its immediate as well as longer-term emissions reduction objectives by “promoting reductions of emissions in a cost-effective and economically efficient manner”.

The main features of the EU ETS are the emission cap (a ceiling on the maximum amount) and the trading of EU emission allowances (EUAs). The cap guarantees that total emissions are kept to a pre-defined level (and does not rise above it – in the period for which the cap applies). Covered installations have to submit an EUA for each tonne of carbon dioxide equivalent (CO2 eq) they emitted during a year.

EUAs are allocated for free or they are auctioned. The trading system offers flexibility to the businesses covered by the scheme as they can decide on taking action or buying EUAs depending on the EUA price. Emitters who have reduction costs lower than the price are encouraged to take action. Emitters with high reduction costs can buy EUAs and postpone their own action thereby complying with the GHG policy more cheaply than they otherwise would have been able to (if, for example, all emitters had to cut emissions by the same ratio).

For accurate tracking of EUAs, participants of the EU ETS open up an account in the Union registry. Anyone possessing an account is able to buy or sell EUAs irrespective of whether they are covered by the EU ETS or not. Trading does not require brokers and can be directly conducted by buyers and sellers through organized exchanges or via intermediaries.

The origins of the EU ETS can be traced back to 1992 when 180 countries agreed to avoid dangerous level of human made global warming and signed the United Nations Framework Convention on Climate Change (UNFCCC). As a means of specifying action to be taken as part of this global joint effort, the Kyoto Protocol (KP) was consequently agreed upon in 1997. The KP introduced two principles essential for the establishment of the EU ETS:

1> It contained absolute quantitative emission targets for industrialised countries and

2> Included a set of so-called flexible mechanisms, which allowed for the option to exchange emission units between countries as an International Emissions Trading system.

The EU (then consisting of only 15 Member States) agreed jointly under the Protocol to an 8% reduction of GHG emissions from 1990 levels in the period 2008 to 2012. At that point in time, it however, lacked the policy instruments to bring about this reduction. Internal debates on plans to introduce a carbon or energy tax had not proven to be successful. Several countries were moving ahead with national emission reduction policies (such as support for renewable energy), but others were waiting for common and coordinated policies and measures to be introduced EU wide. In this general context, the European Commission (EC) started elaborating a proposal for an EU emission trading system to tackle the emissions from key economic sectors (especially energy and industry). As a result of these deliberations, the EU ETS was instituted as one of the key policy measures to reach the Kyoto targets. Currently, it covers the 28 Member States and since 2008, the neighbouring countries of Iceland, Lichtenstein and Norway.

There EU ETS is organised in trading periods (or phases), of which four are currently decided and more may follow. Currently the system is in its third period. Each of the four is described below as follows:

Phase 1: 2005-2007

The European Parliament (2003) passed a law to set up the EU ETS in October 2003 and regulated the first and second trading phase. The first phase of the EU ETS was a pilot phase to test the system. The Member States had the freedom to decide on how many EUAs to allocate in total as well as to each installation in their territory by preparing national allocation plans (NAPs). Almost all EUAs were allocated for free and were based on historic emissions called grandfathering. In this phase, CO2 emissions were covered from installations for power and heat generation and in energy intensive industrial sectors like iron, steel, cement and oil refining, etc. The penalty imposed on the companies for non-compliance was 40 Euro per tonne of CO2.

This initial phase was able to establish a price for EUAs, free trade throughout the EU and the infrastructure for monitoring, reporting and verifying (MRV) actual emissions from the covered installations. Approximately 200 million tonnes of CO2 or 3% of total verified emissions were reduced due to the ETS at nominal transaction costs. However, after the first year of operation, when real world emission data started to be published for the first time, it became obvious that too many EUAs had been allocated to businesses, leading to an oversupply of EUAs and a consequent fall in their price, eventually to zero at the end of the period.

Phase 2: 2008-2012

Since phase two was concurrent with the first commitment period of the Kyoto Protocol, the EU imposed a tighter emission cap by reducing the total volume of EUAs by 6.5% compared to 2005. In this phase Iceland, Norway and Liechtenstein joined the EU ETS and the scope was amended to include nitrous oxide from nitric acid production from several Member States. In addition, from 1 January 2012 onwards, the scheme also included flights within the borders of the EU ETS countries. Up to 10% of the allowances could be auctioned by the Member States instead of free allocation. The penalty for non-compliance rose to 100 Euro per tonne of CO2eq. Businesses were allowed to use credits from the Kyoto Protocol’s Clean Development Mechanism (CDM) and Joint Implementation (JI) leading to a total of 1.4 billion tons of CO2 equivalent credits on the market (with the exception of those for nuclear facilities, agricultural and forestry activities). This move was meant to offer cost-effective mitigation options to businesses and it made the EU ETS the main driver of the international carbon market. Yet, the additional credits and the economic crisis of 2008, which reduced emissions from EU companies, resulted in a large surplus of EUAs, causing a fall of the price from 30 Euro to less than 7 Euro.

Phase 3: 2013-2020

The EC (2009) revised the EU ETS for the third phase. The reasons for these modifications were manifold. Firstly, the fall of EUAs during phase two greatly undermined the reliability of the EU ETS. Secondly, the EU ETS did not generate substantial transformations or movement towards renewable energy industries or low carbon technologies as was expected. Thirdly, it was not as cost-effective as initially anticipated. Lastly, it was subjected to several frauds and scams. To deal with the inherent weaknesses of the system, the changes introduced in this phase particularly include the emission cap applying uniformly over the EU to achieve the GHG reduction target more effectively. The cap decreases by 1.74% per year to reduce emissions by 21% in 2020 compared to 2005.

The main allocation method was modified from grandfathering to auctioning as a principle and some remaining free allocation based on benchmarks. In 2013, allowances for more than 40% of all verified emissions were auctioned. The auctioning platforms are accessible to any country that participates in the EU ETS although the auctions take place at a national level. The process of auctioning is supervised by the EU ETS Auctioning Regulation to ensure that they are conducted in an open, transparent, harmonised and non-discriminatory manner. The amended EU ETS Directive instructs that auctions must match criteria like predictability, cost-efficiency, and fair access to auctions and simultaneous access to relevant information for all operators.

Free allocation applies to industrial installations other than for power generation based on benchmarks (BMs). A BM determines the number of free EUAs based on the installation’s output (or input). There is a BM for each product such as for steel, cement or lime. The installations received 80% of the EUAs they would get according to the BM-allocation. This level will be reduced annually to 30% in 2020. Industries at risk of carbon leakage receive 100% of the BM- allocation over the whole trading period.

The main challenge in the third trading period is the large surplus of EUAs transferred from the second to the third trading period leading to an EUA price of only 3-7 Euro. The EU therefore decided to postpone the auctioning of 900 million EUAs to the end of the trading period (so-called backloading, which was adopted only after a drawn out and controversial political process).10 In addition, the European Commission proposed a market stability reserve to be implemented in the next trading period, which should balance demand and supply by adjusting auctioning volumes.

Phase 4: 2021-2030

This phase will begin 1 January 2021 and finish on 31 December 2028 wherein the EC intends to conduct a full review of the EU ETS Directive by the year 2026. In January 2014, the EC had put forward a legislative proposal for a Market Stability Reserve (MSR) as a part of their proposed policy framework for climate and energy for 2030. It had also given indications that it might tighten the EU ETS cap further.

The EU ETS, a cap and trade system for GHGs from energy and industry, was implemented to ensure that the EU would achieve its GHG emission targets in a cost-effective manner. The system offers flexibility to businesses covered by the scheme as they have the choice between reducing emissions and purchasing emissions from other companies depending on the price of carbon. This promotes the realisation of cheap GHG reductions while the costly reduction measures can be postponed.

4. Carbon Pricing on Imported Goods[4]

The European Commission adopted its Communication on the European Green Deal in December 2019. One of the key policies and measures that would be needed to achieve the Green Deal is the proposal for a carbon border adjustment mechanism (CBAM).

This new mechanism would place a carbon price on imports of certain goods from outside the EU, in order to push EU partners to raise their climate ambition and reduce the risk of 'carbon leakage'. This term describes a phenomenon where companies transfer production abroad to countries that have less stringent emission rules in place. Carbon leakage would counteract Europe's efforts to become climate-neutral by 2050, relocating emissions to third countries rather than reducing global emissions. The European Commission is expected to come up with a proposal later in 2021.

1. Regional Greenhouse Gas Initiative (RGGI)[5]

The Regional Greenhouse Gas Initiative (RGGI) is the first mandatory market-based program in the United States to reduce greenhouse gas emissions. RGGI is a cooperative effort among the states of Connecticut, Delaware, Maine, Maryland, Massachusetts, New Hampshire, New Jersey, New York, Rhode Island, Vermont, and Virginia to cap and reduce CO2 emissions from the power sector.

Within the RGGI states, fossil-fuel-fired electric power generators with a capacity of 25 megawatts* or greater ("regulated sources") are required to hold allowances equal to their CO2 emissions over a three-year control period. A CO2 allowance represents a limited authorization to emit one short ton of CO2 from a regulated source, as issued by a participating state. Regulated sources can use a CO2 allowance issued by any participating state to demonstrate compliance in any state. They may acquire allowances by purchasing them at regional auctions, or through secondary markets.

RGGI CO2 cap represents a regional budget for CO2 emissions from the power sector. For 2021, the RGGI cap is 119,767,784 CO2 allowances and the adjusted cap is 100,677,454 CO2 allowances. Post-2020 cap levels have been established through program review and are detailed in the Principles to Accompany Model Rule Amendments. On March 15, 2021, the RGGI States announced the Third Adjustment for Banked Allowances which is applied to the RGGI cap to account for banked CO2 allowances accumulated through the fourth control period. The adjustment is made over a five-year period (2021-2025), as specified in the 2017 Model Rule.

States sell nearly all CO2 allowances through auctions and invest proceeds in energy efficiency, renewable energy, and other consumer benefit programs. These programs are spurring innovation in the clean energy economy and creating green jobs in the RGGI states.

2. Additional Cap-and-trade Program [6]

On 11 August 2017, the Massachusetts Executive Office of Energy and Environmental Affairs (EEA) announced regulation 310 CMR 7.74 establishing a new cap-and-trade system in the state. The system was limited to the electricity sector, covering 21 fossil-based power plants. The system started in 2018 with free allocation of allowances to utilities. From 2019, utilities were required to purchase all their allowances from an auction. The cap-and-trade program was designed to achieve an 80% reduction in emissions from the covered facilities from 8.96 million metric tons in 2018 to 1.8 million metric tons in 2050. The regulation was accompanied by a Clean Energy Standard requiring an increasing share of electricity from clean energy generation (fossil fuels with carbon capture, nuclear, renewables), reaching 80% by 2050.

The additional system covers the same sector as RGGI. Thus, covered facilities under the new system are also covered by RGGI and would have to hold both types of allowances for each ton of emissions. The systems will operate in parallel but not directly interact.

The regulations are part of a broader roll out of regulations in light of the May 2016 ruling from the Massachusetts Supreme Court. The Court held that the Massachusetts Global Warming Solutions Act (2008) compelled the Massachusetts Department of Environmental Protection to impose additional measures to ensure that the state would meet both its 2020 target of reducing emissions 25% compared to 1990 levels and 2050 target of reducing emissions 80% by 1990 levels. In response, Governor Charlie Baker directed the EEA and DEP to coordinate and put in place additional mitigation efforts in the state.

3. Clean Air Rule[7]

On September 15, 2016, Department of Ecology in Washington State adopted emission standards (Chapter 173-442 WAC – Clean Air Rule) to cap and reduce greenhouse gas (GHG) emissions from significant in-state stationary sources, petroleum product producers, importers, and distributors and natural gas distributors operating within Washington.

Parties covered under the Clean Air Rule are required to reduce their covered GHG emissions along an emissions reduction pathway or obtain emission reductions from other covered parties, GHG emissions reduction projects, or out-of-state emissions market programs. The Clean Air Rule covers two-thirds of all in-state GHG emissions including a wide array of public and private sector parties.

Before the Clean Air Rule's emissions reductions could begin taking effect, a 2018 court ruling suspended the rule. On Jan. 16, 2020, the Washington State Supreme Court upheld the portions of the rule that applied to facilities and other fixed soures, but found other portions invalid. The Supreme Court remanded the case to Thurston County Superior Court to determine how to separate the rule.

Although the Clean Air Rule is currently suspended, facilities covered by the Clean Air Rule still are required to report their emissions for the Greenhouse Gas Reporting program. This reporting program is required by Washington law.

1. Carbon Pricing

Carbon pricing in Canada is implemented either as a regulatory fee or tax levied on the carbon content of fuels at the Canadian provincial, territorial or federal level. Provinces and territories of Canada are allowed to create their own system of carbon pricing based on the needs and requirements of their own jurisdictions. Currently, all provinces and territories are subject to a carbon pricing mechanism, either by an in-province program or by one of two federal programs.

Businesses with certain activities in a listed province can register with the CRA to ensure they fulfill their obligations under the Greenhouse Gas Pollution Pricing Act (“the Act”). There are 12 types of registration, which can be mandatory or voluntary depending the type of activities a business performs. Generally, a charge applies on 21 types of fuel delivered, transferred, used, produced, imported or brought into a listed province. It also applies on combustible waste that is burned, such as tires and asphalt shingles, in a listed province, for the purpose of producing heat or energy.In most cases, the charge applies early in the supply chain and is payable by a registered distributor. End users generally have no obligations in respect of the fuel charge. The fuel that they purchase will already have the charge embedded in the price. [8]

In the absence of a provincial system, or in provinces and territories whose carbon pricing system does not meet federal requirements, a regulatory fee is implemented by the federal Greenhouse Gas Pollution Pricing Act (GHGPPA), which passed in December 2018. In provinces where the fee is levied, 90% of the revenues are returned to tax-payers. The carbon tax is levied because of a need to combat climate change, which resulted in Federal commitments to the Paris Agreement. According to NASA's Jet Propulsion Laboratory (JPL), the air today contains 400 ppm of CO2 while the CO2 level average over the past 400,000 years was between 200 ppm and 280 ppm.

Saskatchewan never had a carbon pricing system and other provinces—Manitoba, Ontario, New Brunswick, and Alberta—have opted out of previous provincial carbon tax systems. Revenue from the federal GHGPPA, which came into effect in April 2019, is redistributed to the provinces, either through tax credits to individual residents or to businesses and organizations that are affected by the tax but are unable to pass on the cost by raising consumer prices. [9]

2. Carbon Tax

The federal and provincial governments in Canada (with the exception of Saskatchewan) agreed to establish a consistent Canada-wide price on carbon pollution. The agreement gave provinces flexibility to devise their own policies, as long as they covered the same sources at the same carbon price. If they didn’t, the federal government would step in.

In 2018, all provinces satisfied the federal government’s conditions except for Saskatchewan, Manitoba, Ontario and New Brunswick, where the federal “backstop” carbon tax is being applied. Although the federal carbon tax is being applied in only those four provinces as of April 1, 2019, residents of other provinces are also paying an equivalent tax — and in some cases have already been doing so for many years.[10]

Due to the existence of the federal carbon tax, residents of Alberta, Ontario, Manitoba and Saskatchewan can receive a tax credit called the Climate Action Incentive (CAI) – an effort to protect the environment while making the shift to sustainable actions more affordable. This is because the carbon tax (or “fuel charge”) is added directly to the cost of people’s gas when people fill up at the pumps and to people’s home heating bills. The fuel charge gives people the incentive to make cleaner choices and encourages businesses to find clean solutions – which benefits us all as it protects the environment and helps grow the economy. The goal of the CAI is to offset the cost of the fuel charge and put some money back in people’s pocket.[11]

1. Climate Active Certification[12]

Climate Active is a partnership between the Australian Government and Australian businesses to encourage voluntary climate action. Leading organisations are choosing to reduce their climate impact to zero by becoming carbon neutral. Climate Active certification is awarded to businesses that have credibly reached net zero emissions. Certification is available for buildings, events, organisations, precincts, products and services.

Certification showcases people’s carbon neutral status and helps the community take individual action by selecting brands showing climate leadership. Certification for buildings is available through the National Australian Built Environment Rating System (NABERS) or the Green Building Council of Australia. Certification for events, organisations, precincts, products and services is available through the Department of Industry, Science, Energy and Resources. For people’s entity to be certified people must meet the requirements of the Climate Active Carbon Neutral Standard.

To become carbon neutral, businesses and organisations need to:

•calculate the greenhouse gas emissions generated by their activity, such as fuel or electricity use and travel;

•reduce these emissions as much as possible by investing in new technology or changing the way they operate;

•offset any remaining emissions by purchasing carbon offset units.

Once business have cancelled out their emissions, they have reached a state called ‘carbon neutral’ and can be certified.

To become certified businesses, companies may need to enter into a licence agreement with the government. The licence agreement includes:

•Terms and conditions for certification against the Climate Active Carbon Neutral Standard and use of the Certification Trade Mark

•glossary and interpretation

•fee schedule

•reporting schedule

•validation schedule

2. Emissions Reduction Fund[13]

The Emissions Reduction Fund is a voluntary scheme that aims to provide incentives for a range of organisations and individuals to adopt new practices and technologies to reduce their emissions. It is enacted through the Carbon Credits (Carbon Farming Initiative) Act 2011, the Carbon Credits (Carbon Farming Initiative) Regulations 2011 and the Carbon Credits (Carbon Farming Initiative) Rule 2015.

A number of activities are eligible under the scheme and participants can earn Australian carbon credit units (ACCUs) for emissions reductions. One ACCU is earned for each tonne of carbon dioxide equivalent (tCO2-e) stored or avoided by a project. ACCUs can be sold to generate income, either to the government through a carbon abatement contract, or in the secondary market.

To ensure these emissions reductions are not displaced significantly by a rise in emissions elsewhere in the economy, the Emissions Reduction Fund also includes a safeguard mechanism, which encourages large businesses to keep their emissions within historical levels. The safeguard mechanism came into effect on 1 July 2016.Following the 2017 review of climate change policies, and extensive consultation during 2018, the safeguard mechanism was amended in March 2019. The amendments were designed to make the mechanism fairer and simpler. Changes apply to baselines that commence from 1 July 2018.

3. Mandatory renewable energy target [14]

Australia's Renewable Energy Target (RET) is a Federal Government policy designed to ensure that at least 33,000 gigawatt-hours (GWh) of Australia's electricity comes from renewable sources by 2020. The RET consists of two main schemes:

A. The Large-scale Renewable Energy Target (LRET) requires high-energy users to acquire a fixed proportion of their electricity from renewable sources. This occurs in the form of large-scale generation certificates (LGCs), which are created by large renewable energy power stations (such as solar or wind farms) and then sold to high-energy users who must surrender them to meet their obligations under the LRET.

B. The Small-scale Renewable Energy Scheme (SRES) provides a financial incentive for individuals and businesses to install small-scale renewable energy systems such as rooftop solar, solar water heaters and heat pumps. This occurs in the form of small-scale technology certificates (STCs), which are issued up front for a system’s expected power generation (based on its installation date and geographical location) until the SRES expires in 2030. Similar to the LRET, large energy users are required to purchase a fixed proportion of STCs and surrender them to meet their obligations under the RET.

In September 2019, the Clean Energy Regulator announced that Australia had met the LRET more than a year ahead of schedule.While the LRET’s 33,000 GWh target was met in September 2019, the scheme will continue to require high-energy users to meet their obligations under the policy until 2030.As more renewable energy is produced beyond the 33,000 GWh target, the number of LGCs generated will continue to increase, leading to an oversupply in the market that will significantly reduce their value. Futures markets indicate that LGC prices will fall significantly over the next ten years, with some analysts predicting that their value will fall to zero by the time the RET expires in 2030.

The SRES is scheduled to run until 2030, with the level of subsidy available falling each year between now and the end of the scheme. There is no limit on the amount of renewable energy that can be produced under the SRES.However, a July 2018 report by the Australian Competition and Consumer Commission into electricity prices recommended that the SRES be abolished in 2021 rather than 2030 to reduce electricity costs.

The RET was reviewed by the Government and reduced in June 2015 from the previously legislated 41,000 GWh to 33,000 GWh. The deal was a compromise brokered by the Clean Energy Council following 15 months of lost investment confidence caused by the review of the policy.

4. Carbon Pricing Scheme was introduced and then abolished

A carbon pricing scheme in Australia was introduced by the Gillard Labor minority government in 2011 as the Clean Energy Act 2011 which came into effect on 1 July 2012. Emissions from companies subject to the scheme dropped 7% upon its introduction. The plan was it would transition to a cap-and-trade emissions trading scheme three years later, linking Australia to international carbon markets.[15]

But it never got that far. After one of the most divisive elections in Australian history, in which the opposition Liberal-National coalition campaigned to “axe the tax”, they did just that when elected and the carbon price was repealed on July 17th, 2014.

Australia’s Labor government under prime minister Julia Gillard had brought in the tax in the first place because the country has one of the highest per capita carbon emissions in the world.

To offset the impact of the tax, Labor reduced income tax and increased welfare payments to cover expected price increases. It also introduced compensation for some affected industries. When the carbon price was repealed, the Australian National University estimated the scheme had cut carbon emissions by about 17 million tonnes in 2013, the biggest annual reduction in 24 years of records.

But scaremongering on the carbon price was a major contributor to the coalition winning government in a landslide in 2013. Then prime minister Tony Abbott said getting rid of the tax would save people $550 (€485) a year. This figure was widely disputed, but electricity and gas prices did fall by an estimated 7 and 5 per cent respectively. But Australia’s emissions went up again. With 0.3 per cent of the world’s population, it produces 1.8 per cent of the world’s greenhouse gases. The latest per capita figure for C02 emissions in Australia was 17.22 tonnes, more than three times the Irish figure. [16]

The popular policy options introduced by other countries to reduce greenhouse gas emissions include[17]:

1. Cap and Trade Scheme

A cap and trade scheme has—as its name suggests—two elements. The first is a limit on the quantity of pollution that can be emitted: the cap. The second is the facility to trade the limited number of carbon permits, after they are issued through an auctioning process. Companies are required to provide to the authorities permits equivalent to the amount they emit. Companies increasing their emissions will need to buy more permits, either at the initial auctions or in the market. Companies cutting their emissions need to buy fewer permits and may have surplus permits they can sell in the market. A cap and trade scheme thereby offers market participants the opportunity for 'least cost abatement'.

A cap and trade scheme is the preferred policy approach of the Australian Government and forms the basis of the Carbon Pollution Reduction Scheme. The European Union (EU) introduced a cap and trade scheme in January 2005 which included 15 of the Union's 27 nations and covered nearly half the EU's emissions.

2. Carbon Tax

At its simplest, a carbon tax would work by taxing emissions at a constant rate. For example, a company would pay a set amount in tax for each tonne of carbon dioxide it emits. A carbon tax would not establish a cap on national emissions per se. However, a carbon tax is designed to discourage the consumption of emissions-intensive goods and services. Companies will reach a point at which it becomes more cost effective to undertake abatement and/or adaptation than incur the tax.

A carbon tax is favoured by its proponents both for its simplicity and for providing investor certainty. It is simple insofar as it could be universally applied, without sectoral exemptions or compensation. It provides investor certainty because the level of the tax is fixed and known in advance. A cap and trade scheme, on the other hand, is potentially much more complex with the difficult issues of the level of the cap and compensation arrangements to negotiate. There is also less predictability and more volatility in carbon prices under a cap and trade scheme which may affect investor confidence.

3. Regulation and Incentives

An alternative form of government intervention to address climate change would be in the form of a mixture of 'command and control' style regulation or by providing incentives. A number of such measures have been proposed for dealing with climate change, either to sit alongside a market based approach as a 'complementary measure', or as measures which can provide an alternative to a market based approach.

Several examples of such responses are already in existence in environmental regulation at Commonwealth and state/territory level. Examples which have been raised with the committee include mandating tighter energy efficiency standards and labelling in appliances, vehicles and new buildings. Other examples might include a moratorium on future construction of coal fired power stations; mandating the purchase of renewable energy through measures such as the Renewable Energy Target. Incentives include funding for research and development or pilot projects, feed-in tariffs, subsidies (aimed at householders or industry) or rebate schemes to cover the cost of installing new technology (such as solar panel rebate schemes).

[1]https://www.europarl.europa.eu/news/en/headlines/society/20190926STO62270/what-is-carbon-neutrality-and-how-can-it-be-achieved-by-2050

[2]https://taxfoundation.org/carbon-taxes-in-europe-2020/

[3]https://climatepolicyinfohub.eu/eu-emissions-trading-system-introduction

[4]https://www.europarl.europa.eu/committees/en/carbon-border-adjustment-mechanism/product-details/20201009CDT04181

[5]https://www.rggi.org/

[6]https://icapcarbonaction.com/en/news-archive/483-massachusetts-introduces-additional-cap-and-trade-system

[7]https://ecology.wa.gov/Air-Climate/Climate-change/Greenhouse-gases/Reducing-greenhouse-gases/Clean-Air-Rule

[8]https://www.canada.ca/en/revenue-agency/campaigns/pollution-pricing.html

[9]https://en.wikipedia.org/wiki/Carbon_pricing_in_Canada

[10]https://globalnews.ca/news/5125670/how-the-carbon-tax-works/

[11]https://www.hrblock.ca/blog/what-is-the-climate-action-incentive-heres-how-it-affects-your-taxes/

[12]https://www.industry.gov.au/regulations-and-standards/climate-active

[13]http://www.cleanenergyregulator.gov.au/ERF/About-the-Emissions-Reduction-Fund

[14]https://www.cleanenergycouncil.org.au/advocacy-initiatives/renewable-energy-target

[15]https://en.wikipedia.org/wiki/Carbon_pricing_in_Australia

[16]https://www.irishtimes.com/news/environment/how-not-to-introduce-a-carbon-tax-the-australian-experience-1.3746214

[17]https://www.aph.gov.au/Parliamentary_Business/Committees/Senate/Former_Committees/climate/report/c03

京公网安备 11010502044998号

京公网安备 11010502044998号